Company & Trust Account

Where term-based accounts get personal: your savings is your opportunity to earn

It’s not always easy knowing what to do with your money. Particularly when it’s your life savings or a big lump sum that means the world to you. That’s where TermPlus has you sorted, as we empower your money to earn more through high-yield, term-based personal accounts.

Income paid monthly

Quick & Easy online application

No Setup or Monthly Account Fees

What Is the TermPlus Advantage?

Easy access

Managing your money is effortless, with quick and convenient access on a state of the art secure platform.

Choose how you earn

Priority Income

We provide an extra pool of income returns to support our Target Rates for your account.

Income stabilisation

We always calculate your Target Rate Income on the total Invested Amount (including any reinvestments of past Income). The monthly payment of accrued Target Rate Income is not guaranteed and is subject to TermPlus generating sufficient return.

Savings support

At the end of your Term, if the Closing Balance of your Term Account, plus any Income already paid or accrued to you during the course of your Term, is lower than your total Invested Amount, the Support Account will top up your account balance by up to 5% of your total Invested Amount.

Trusted partners with global expertise

We collaborate with the very best to access reliable performance and global expertise.

Floating Rates

By linking Target Rates to the cash rate, we aim for Account Holders to stay one step ahead. Target rates are calculated by reference to the RBA Official Cash Rate plus a fixed spread (‘Added Rate’), expressed on an annualised basis.

Net Target Rates

TermPlus target rates are a net return to Account Holders. There are no additional fees and charges over the Target Rates.

Your Money, Making Money

- Let your savings generate wealth for you.

- Designed to deliver capital stability and reliable monthly income.

- Take your monthly income as a direct payment into your nominated bank account, or reinvest it for compounding growth.

Make your money work smarter!

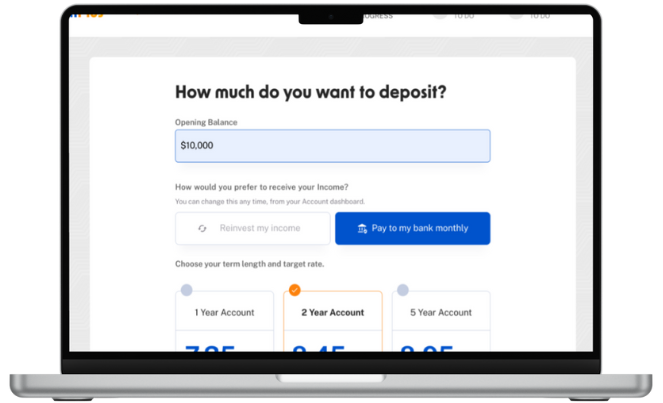

Income Calculator

How much do you want to deposit?

(includes reinvested Target Total Income)

How would you prefer to receive your Income?

my income

bank monthly

- Earns income daily

- Paid to you monthly

- Built-in Savings Support

(includes reinvested Target Total Income)

How would you prefer to receive your Income?

my income

bank monthly

- Earns income daily

- Paid to you monthly

- Built-in Savings Support

(includes reinvested Target Total Income)

How would you prefer to receive your Income?

my income

bank monthly

- Earns income daily

- Paid to you monthly

- Built-in Savings Support

*Calculations provided are for indicative purposes only and have been subject to rounding adjustments. The above quoted Target Rates are those current as at today and are merely objectives, which may change during the course of the Term. Please refer to the Product Disclosure Statement (‘PDS’) for TermPlus for an explanation of the Target Rates and other terms used on this website. Any revised Target Rate for each Term will be detailed on the website: www.termplus.com.au and applied to both new and existing Term Accounts. There is a risk that TermPlus may not be successful in achieving the Target Rates. Whilst TermPlus Accounts provide for Priority Income Entitlement, Income Stabilisation and Savings Support (‘Support Mechanisms’) to support the delivery of TermPlus Account objectives, none of Pengana Capital Limited (and Pengana Credit Pty Ltd) and their associates, shareholders, agents, managers, advisers or delegates guarantee the performance of TermPlus. Account Holders’ capital is not guaranteed. Like all investments, even with Support Mechanisms, TermPlus’ investments carry risks, and if these risks eventuate, Account Holders may lose some or all of their capital invested in TermPlus. The Target Rate is not guaranteed, is not a forecast, and may not be achieved. The Target Rates are calculated off the RBA Cash Rate plus a fixed percentage spread. The RBA Cash Rate can change from time to time. An investment in an Account is not a bank deposit or a term deposit with a bank. Past performance is not a reliable indicator of future performance. The Target Rate is a net amount. The financial product described herein will be issued by Pengana Capital Limited in its capacity as trustee of TermPlus ARSN 668 902 323. Before deciding whether to acquire, or to continue to hold the product, you must read the PDS available on this website and consider whether the product is right for you. You should also read the Target Market Determination which describes who the financial products mentioned herein, may be appropriate for.

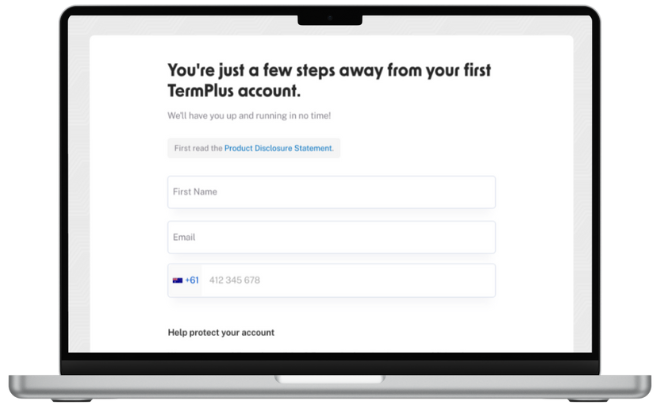

Getting Started Is Easy

1. Verify your details

Confirm your identity and select your account type.

2. Tailor your Term

Choose your investment amount, Term and Income preference.

3. Deposit your funds

See your savings go to work for you, month-to-month.

Your Data Is Important to Us

Two-factor authenticated accounts

KYC/KYB/AML compliant

Data encryption

No fuss

No fuss

We Aim to Please

20+ years investing for Australians

Backed by industry-leading partners with decades of experience and global reach, TermPlus delivers a robust solution for putting your savings to work.

People’s Choice Winner:

Finder Awards - Australia’s Best Investment Innovation 2025

“I have now opened 4 accounts with Term Plus for both 2-year and 1-year terms, so staggering the maturity dates. The process is very straightforward and the monthly income simple to review. I choose to have the monthly payments reinvested. So far I have been very pleased and consider Term Plus offers an excellent means of diversifying the investments held in my SMSF, with a realistic target rate and the reliability of its Pengana managers.”

David C, 78 (SA)

“I’ve been with TermPlus about six months, and have to say that people are very helpful. Plus, I’m happy with the income rate and my return each month. I just wish I came across this long time ago! Considering what is out there, it’s not much at all. Everyone wants to get the best for their money. So far, I like to say, I’m very happy and I hope it stays that way thank you.”

Patrick Pace, 65 (NSW)

Built with You in Mind

Created and powered by Pengana Capital Group in association with Mercer, TermPlus taps into the dynamic world of global Private Credit to deliver leading Term Accounts with built-in layers of protection for its customers.

- Get more from your money

- Save for retirement

- Plan your next big getaway

- Make the home extension happen

- Put away for a rainy day

- Get closer to that dream purchase

- Fund your retirement lifestyle with generous and reliable Target Rates

*Source: BCG consumer sentiment survery September 2023.

Frequently asked questions

TermPlus is not a bank. TermPlus is a provider of high yield online term accounts. These term accounts offer monthly income with target rates from 7.35%* p.a. that can be paid directly into your bank account each month, or you can choose to reinvest your monthly income for compounding returns.

We work closely with leading investment institutions such as Pengana Capital Group and Mercer.

Our goal is to make wealth-building simple, rewarding, and reliable. Open your account today to see how your savings can work harder for you.

TermPlus invests in a highly diversified, and professionally constructed, global private credit portfolio. This is managed by trusted institutions, and delivers competitive returns in the form of monthly income.

Ready to earn more without the stress? Open your TermPlus account today.

To keep them relevant, TermPlus Target Rates are determined using a fixed margin above the RBA cash rate. The fixed margin varies depending on the length of the Term.

As the RBA changes the cash rate from time to time, so the Target Rate will fluctuate with those changes. The fixed margin above the RBA cash rate does not change.

This enables us to keep income payments relevant and reliable over the course of your term.

Since inception, TermPlus account holders have received 100% of their targeted monthly income payments, and we have never missed a monthly payment to account holders.

While it’s important to note that past performance is not a reliable indicator of future performance, and the value of all investments can go up or down, the three layers of protection offered by TermPlus can help fund monthly payments and repayment of your investment.

TermPlus generates returns for customers from the global private credit sector. Global private credit is an unlisted asset class, and has generally been uncorrelated with listed stock markets – that is, historically there has not been a direct connection between stock market performance and global private credit performance.

While it’s important to note that past performance is not a reliable indicator of future performance, and the value of all investments can go up or down, the three layers of protection offered by TermPlus can help fund monthly payments and repayment of your investment.

You can also read more about how we generate monthly returns, and our in-built layers of account protection HERE.

The TermPlus TMDs and PDS are also available HERE.

TermPlus offers target rates determined by the RBA Cash Rate plus the addition of a fixed spread. As the RBA Cash Rate can potentially go up or down over the course of a term, the target rates will vary in line with the RBA Cash Rate Changes.

Don’t settle for less, open your account and start earning today.

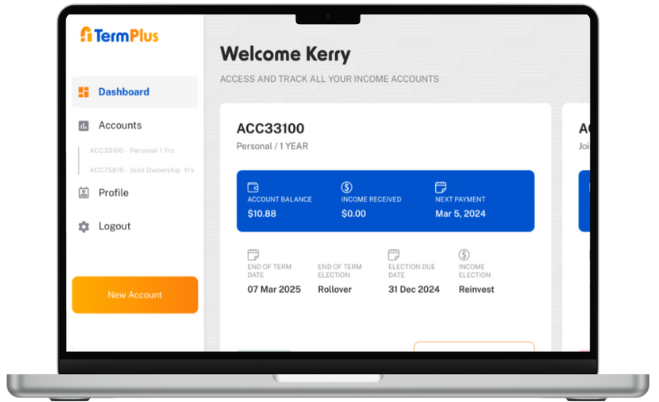

Easy. Quick. Seamless. Your TermPlus Account has its own easy-to-use account dashboard from where you can manage and track your applications, get an overview of all your term accounts, track your earnings and access tax statements etc.

TermPlus charges no setup fee, no monthly account fee or transaction fees. All underlying management fees are already factored into our target rates. This means you can enjoy total clarity from the start. Ready for straightforward growth? Open your account today.

Your Income payments are based on the starting balance of your Account, and any subsequent reinvested income payments (should you choose to reinvest some of your monthly income).

As this is a fixed term account, no additional funds can be added or withdrawn from your account over the course of your fixed term.

If you would like to add new funds to earn Income, this can easily be done by opening another Term Account using the ‘add account’ button on your dashboard.

You have 2 choices at the end of the Term.

- Roll your account balance into a new Term of your choice, to continue receiving monthly income payments.

- Withdraw your closing balance back into your bank account.

‘End of term’ elections need to be made by the due date that is noted on your account in the customer dashboard.

Sure do, and they’re growing – just head over here: https://termplus.com.au/reviews/

TermPlus has been featured in several highly regarded news and investment publications that have recognised our innovative accounts, and commitment to customer-centric solutions. These articles offer valuable insights into who we are, what we do, and how we’re reshaping the term account landscape.

We encourage you to explore these articles to learn more about our mission, values, and how we’re redefining investment opportunities.

The TermPlus TMDs and PDS are also available HERE.

Have additional questions? Our team is always here to help!

Need to Know More?

Click here to contact our client service team or simply call 1300 883 881 for assistance.